When it comes to managing debts, especially when dealing with loans, individuals often face various hurdles. One of the solutions that borrowers might consider is loan settlement. This article will explore what loan settlement means, how it works, and importantly, the implications it can have on your CIBIL score.

Understanding Loan Settlement

Definition of Loan Settlement

Loan settlement refers to the process of negotiating with a lender to reduce the outstanding loan balance. In simple terms, it involves reaching an agreement between the borrower and the lender where the borrower pays a lump sum amount that is less than the actual debt owed. This is common in situations where borrowers are facing financial difficulties and cannot repay the entire amount.

The Process of Loan Settlement

1. Assessment of Financial Situation

The borrower needs to evaluate their finances to determine the extent of their inability to repay the loan.

2. Contacting the Lender

The borrower approaches the lender to discuss their financial hardship and expresses a desire to settle the loan.

3. Negotiation

Both parties negotiate terms—specifically, how much the borrower can pay as a settlement amount.

4. Agreement

Upon reaching an agreement, the borrower pays the agreed settlement amount, and the lender marks the debt as settled.

Who Should Consider Loan Settlement?

Loan settlement can be an appropriate option for individuals facing significant financial distress or those who have fallen behind on personal loan EMI. However, it’s crucial to understand that this should not be the first step when dealing with debt but rather a last resort when other options have been exhausted.

Understanding CIBIL Score

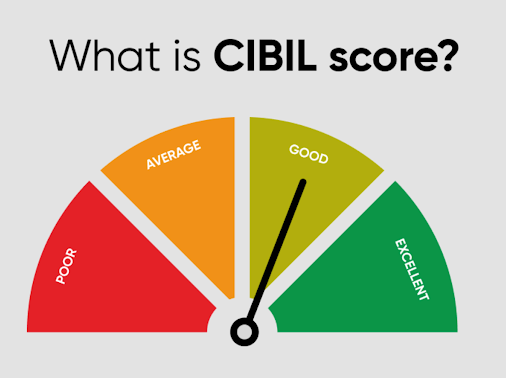

What is a CIBIL Score?

A CIBIL score is a three-digit number that represents an individual’s creditworthiness. This score ranges from 300 to 900, with scores above 750 generally considered good. It is primarily determined by your credit history, outstanding debts, and payment patterns.

Importance of CIBIL Score

Your CIBIL score profoundly impacts your ability to secure future loans or credit facilities. Banks and financial institutions use this score to evaluate your credit risk. A high score improves your chances of loan approval, higher loan limits, and better interest rates, while a low score can result in loan rejections or increased costs.

The Impact of Loan Settlement on CIBIL Score

Negative Implications of Loan Settlement

1. Decrease in CIBIL Score

When a loan is settled rather than fully paid off, it is recorded as a partial repayment to credit bureaus, which typically leads to a significant dip in your CIBIL score. This is because it indicates to lenders that you were unable to adhere to the original loan agreement.

2. Credit Report Notation

The settlement status will be recorded on your credit report. A notation indicating that the loan was settled can impact your chances of gaining access to future credit options.

Time Frame for Recovery

While the immediate impact of a loan settlement is negative, it’s essential to note that the effects are not permanent. Over time, with responsible credit behavior, it is possible to improve your credit score. Generally, it may take anywhere between six months to two years of good credit management to see a significant recovery.

Managing Personal Loan EMIs After Settlement

Create a Realistic Repayment Plan

After a loan settlement, borrowers should create a budget to ensure they can meet their essential financial obligations. If you have other loans, the focus should be on ensuring timely payments of future EMIs. This commitment will positively affect your CIBIL score over time.

Avoid Further Borrowing

While you may feel tempted to secure a loan to plug immediate financial gaps after a settlement, it’s advised to avoid this until your financial situation stabilizes. Further borrowing can increase your debt burden and negatively affect your CIBIL score.

Alternative Solutions to Loan Settlement

Debt Restructuring

Instead of heading toward settlement, consider negotiating a debt restructuring plan with your lender. This may include extending the loan term or lowering interest rates, which could make managing your payments easier.

Credit Counselling

Engaging with a credit counselling service can provide tailored advice on managing your debts effectively, potentially avoiding the need for a loan settlement.

Personal Loan Refinancing

If you are struggling with high EMIs, refinancing a personal loan may be an option worth considering. By securing a lower interest rate or extending the loan term, your monthly outgoings might become more manageable without impacting your credit score negatively.

Conclusion

Loan settlement can seem like an attractive option for those facing financial difficulties, but it’s vital to understand the potential ramifications on your CIBIL score. A reduced score can hinder future financial opportunities, making it crucial to seek other avenues for managing debt first. Ultimately, it’s essential to evaluate your options thoroughly and consider long-term effects when making decisions about debt management. Engaging in healthy credit practices post-settlement can help you rebuild your score over time, ensuring better financial prospects in the future.